Estate Planning – Don’t Delay!

•We’ve all read or heard the stories. Someone passes away without a will, and potential heirs sharpen their knives in a free-for-all that can take years to play out in court. The emotional toll is immeasurable, with relationships incurring irreparable harm that can last generations.

Or, as highlighted just a few days ago in the Wall Street Journal, “The Brady Bunch Breaks Down: Estate Fights Tear Stepfamilies Apart—In Standard Estate Plans, a Surviving Spouse Often Has No Legal Obligation to Stepchildren,” failure to adequately plan can lead to devastating consequences for blended families.

“The default rules are out of touch with today’s family structures,” according to Danaya Wright, a University of Florida law professor.

In T.V. land, Carol would not forsake Mike’s three boys if her beloved husband passed first. Even their housekeeper Alice, who became part of the family, would have been taken care of.

But T.V. and real life don’t always line up. In today’s world, Greg, Peter, and Bobby could be left high and dry without a concrete written plan. The implications are real and immediate.

Without a will or trust, the state chooses how your estate is divided and who will take care of your minor children.

Only one-third of Americans have a will or a plan to distribute their assets after they die, according to a new survey from Senior Living Referral Service Caring.com.

According to a survey by USLegalWills.com, almost 9% had an out-of-date will, while a staggering 63% had no plan in place. Put another way, over two-thirds of Americans have a big hole in their financial plan. It’s crucial not to be part of this statistic!

But, you may ask, the wealthy make up a small percentage of those with significant assets, right? The wealthy hire the best and brightest to manage their affairs, right?

Well, not always. One in five Americans with investible assets of $1 million or more don’t have a will, according to a recent Charles Schwab survey.

Legendary talk show host Larry King used a short, handwritten note, with typos, to update his will.

“This is my Last Will & Testament. It should replace all previous writings,” said the letter. “In the event of my death, any day after the above date, I want 100% of my funds to be divided equally among my children Andy, Chaia, Lary Jr Chance & Cannon.”

That’s a recipe for a long and drawn-out court battle.

Whether young or old, the famous have passed on without written plans, including Aretha Franklin, Prince, Michael Jackson, Bob Marley, Jimi Hendrix, Sonny Bono, Kurt Cobain, and Amy Winehouse. Even Abraham Lincoln, who was a lawyer, didn’t have a will.

Valued at $80 million, the fight over Hendrix’s estate lasted over 30 years. Without a clear plan, your heirs could quickly turn to lawyers and the court.

But let’s be clear. Estate planning isn’t only for the wealthy.

Dying intestate—without a will—will have consequences no matter where you live. How your affairs are settled depends on the state in which you reside.

But it is especially painful if there are unmarried partners, stepchildren, and even a parent’s own child who may lose an inheritance.

Stop procrastinating

If you have recently crafted an estate plan with an estate attorney or have updated your will, a hearty congratulations goes out to you. A holistic financial plan includes a plan of succession.

If not, let’s get started.

Estate planning requires us to do something today that hasn’t happened yet.

Without a plan, your loved ones will be forced to guess your intentions against the backdrop of an already difficult situation. Even if potential heirs are on good terms, money has a way of creating divisions.

Key takeaways

- Common estate planning documents include wills, trusts, powers of attorney, and living wills.

- Everyone can benefit from having a will, no matter how small their estate.

- Online estate planning services offer basic packages for less than $200 (more in a moment).

- Estate planning attorneys can cost several hundred dollars per hour.

- Estate plans must be updated after significant life events.

What is a will? It is a legal document stating how you want your executor (the person legally obligated to administer your estate) to distribute your assets after you die.

Your estate will go through probate, the legal process for reviewing the assets of a deceased person and determining who inherits what, whether you have a will or not.

If you have a will, it ensures the executor will honor your wishes.

A will lists your assets, bank and brokerage accounts, property, and more. Without a detailed document, potential heirs may be forced to search for assets spread across states and even countries.

Do you have designated beneficiaries for various accounts, such as IRAs? The beneficiary designation trumps the will.

What is a living will? It is written, legal instructions stating your preferences for medical care if you are unable to make decisions.

What is a trust? A trust is a legal contract that allows another person (the trustee) to hold property for you (the grantor).

This is typically so the beneficiaries (individuals or institutions who stand to inherit something) can use the property at some point in the future.

What is a living trust? You create a living trust to hold assets before and after your death.

What is a testamentary trust? It is a trust created by the will and only becomes effective after the grantor’s death.

Power of attorneys

A durable power of attorney enables your agent to act on your behalf if you become ill or are unable to make decisions.

For example, a durable financial power of attorney allows your agent to manage your financial affairs if you become incapacitated or are unable to make decisions on your own.

A durable medical power of attorney allows you to appoint someone to make decisions about life-prolonging care, treatment, services, and procedures.

DIY hazards

Talking to a representative at Home Depot about your next painting project is commendable. Do-it-yourself (DIY) estate planning is cheap. It’s hard to argue against cheap unless you make unwanted mistakes that invalidate your wishes.

Estate planning is complex, and it helps to have professional advice. Saving a few dollars today can cost your heirs pain and anguish that could have easily been avoided.

We lost one of our dearest clients recently- we will call her Jane. Jane had been very adamant about keeping her estate plan to herself, only sharing with us her beneficiary designations.

Upon her passing, we learned from her daughter (the designated executor of her will) that her mother wanted a large portion of her retirement plan assets to be divided between her grandchildren per the will’s instructions. Unfortunately, Jane had directed us to list her daughter as the beneficiary of the retirement plans. Her daughter is in her 50s and in her prime earning years. Jane’s daughter will have to take these retirement funds, withdraw them, then divide them among the grandchildren as listed in the will.

The unfortunate part of this plan is that Jane’s daughter will have to pay taxes on all of the withdrawals at a much higher tax bracket than if the funds were given directly to the grandchildren via beneficiary designations.

If Jane had used an estate planning attorney and shared her will with us, her financial planning team, she could have transferred these funds in a much more tax efficient way.

Prepare your heirs

You don’t have to divulge the details, but informing beneficiaries opens the financial lines of communication, reducing the odds of a contested will. In addition, it promotes family unity at a time that can be exceedingly difficult.

Surprises breed resentment, and resentment may lead to unwanted consequences.

We recognize that estate planning is a personal process. In some cases, you may feel overwhelmed, especially if you have a large family, a blended family, or a family that has gone through separations and divorce.

Our objective is to initiate a dialogue, assist you in developing a plan, or motivate you to revise an existing one if the need has arisen.

We are always available to address any questions you may have.

Failure to act puts your legacy at risk.

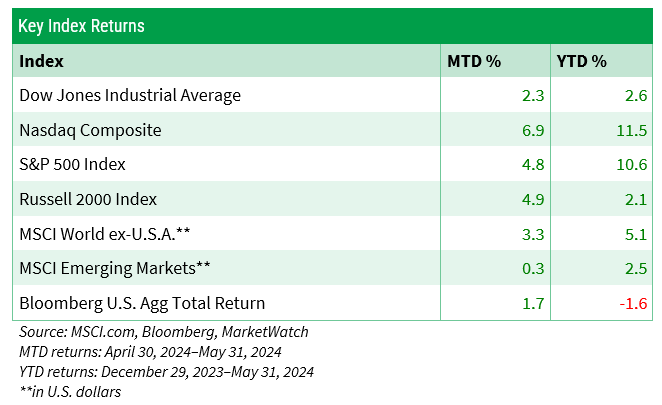

Successful investing

2022 was a difficult year for investors, and we recognize that detours on the road to your financial goals are not uncommon.

Legendary investor Warren Buffett opined, “Every decade or so, dark clouds will fill the economic skies, and they will briefly rain gold. When downpours of that sort occur, it’s imperative that we rush outdoors carrying washtubs, not teaspoons.”

Our goal is not to time markets, and Buffett would agree. He counsels that “it’s far better to buy a wonderful company at a fair price than a fair company at a wonderful price.”

But he recognizes that stocks aren’t immune to significant pullbacks. He would caution that a bear market isn’t the time to bail on stocks.

In his 2013 letter to shareholders, he noted, “The goal of the non-professional should not be to pick winners—neither he nor his ‘helpers’ can do that—but should rather be to own a cross-section of businesses that in aggregate are bound to do well.”

2022 may have tried your patience, but patient investors were rewarded in the following year. The skies cleared, and those who were invested in that “cross-section of businesses” were handsomely rewarded.

In 2024, a well-diversified portfolio has continued to perform well. But we are also aware that pullbacks can never be discounted.

Adhering to a long-term strategy takes discipline. And much like the turtle in the fable of the tortoise and the hare, those who have taken the steady and disciplined road have reaped their rewards.

Yet, we understand that the noise from the 24-hour news cycle can throw up roadblocks, even for the most patient investor.

Avoiding distractions, stay focused

- Skip the fads. Jumping into cryptocurrencies or playing the “meme-stock” game offers the allure of overnight riches. But these trains can turn quickly, and you can end up with big holes in your portfolio that aren’t easily plugged.

- We’re human. Humans sometimes let emotions get the best of them. But we caution you to avoid the temptation to move away from stocks in down markets. Conversely, when stocks are surging, avoid going “all in.” We urge you to maintain the appropriate mix of stocks and income-producing investments.

- Balance and re-balance and re-balance again. For example, a 60/40 portfolio of stocks and income-producing investments will eventually drift out of alignment. A 60/40 may become 70/30 or 80/20. Make adjustments that re-align your portfolio with your long-term strategy and tolerance for risk. Otherwise, you may find yourself in deeper, riskier waters.

While we encourage you to stay with your plan, no plan is set in concrete. When life changes, let’s make adjustments that mirror your new circumstances.

We trust you have found this review to be informative. If you have any inquiries or wish to discuss other matters, please don’t hesitate to contact me or any team member.

As always, thank you for choosing us as your financial advisor. We are honored and humbled by your trust.